On 16 July 2018 the Financial Reporting Council (FRC) published its long awaited update to the UK Corporate Governance Code together with revised Guidance on Board Effectiveness.

On 16 July 2018 the Financial Reporting Council (FRC) published its long awaited update to the UK Corporate Governance Code together with revised Guidance on Board Effectiveness.

The revisions support the government’s vision of restoring trust in the corporate organisations and the broader social reform agenda which aims to improve the standard of living and quality of life for ordinary working people.

In this paper, the Institute looks at the key changes and their relevance to internal auditors.

Summary of Changes

The business secretary, Greg Clark commented that “these changes will drive improvements in how boardrooms engage with employees, customers and suppliers as well as shareholders, delivering better business performance and public confidence in the way businesses are run.”

A full summary of the changes is published by the FRC, in essence it is

- Shorter and easier to navigate

- Focused on the Principles

- Enhanced with new Principles on stakeholder engagement, alignment of strategy, culture and values, board responsibilities regarding workforce policies, refreshing the board and remuneration

- Less onerous (59 principles and provisions compared to 99 previously)

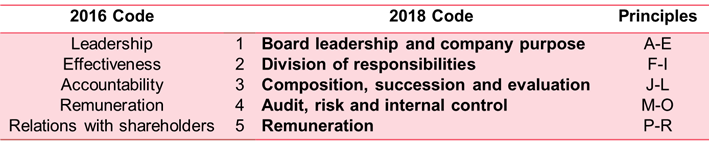

The five section headings have changed under which the Principles and Provisions are listed.

Changes Specific to Internal Audit

Principle M requires the board to establish formal and transparent policies and procedures to ensure the independence and effectiveness of internal and external audit functions and satisfy itself on the integrity of financial and narrative statements.

- Chief audit executives (CAEs) without a direct reporting line to the audit committee should use this principle as a discussion lever to effect change with their audit committee chair. For additional information on what constitutes ‘independence’ refer to the International Professional Practices Framework (IPPF) Standard 1110.

- The principle also introduces formality to ensuring the effectiveness of internal audit that was missing from the previous Code. Again this is an…